The 2017 Tax Cuts and Jobs Act provided a unique opportunity for private investors to defer capital gains on the sale of property and exempt future gain on their new investments from tax.

The catch? Investors have 180 days after the sale of property to invest the proceeds into a qualified opportunity fund.

WHAT THE HECK IS A QUALIFIED OPPORTUNITY FUND?

A qualified opportunity fund is a vehicle (partnership or corporation) that invests in a designated opportunity zone.

WHAT DO YOU MEAN OPPORTUNITY ZONE?

26 US Code § 1400Z–1 points us towards §45D — I’ll spare you from the internal revenue code legal jargon. Essentially, it is a low-income zip code where the poverty rate is at least 20% or median household income is 80% of the statewide median income.

Investors reap three massive benefits:

- Original Gain Deferral: Upon investment of capital gain into a qualified opportunity fund (QOF), the invested gain is deferred from inclusion in the taxpayer’s gross income until the earlier of the taxpayer selling the QOF investment, December 31, 2026, or an “inclusion event”.

- Original Gain Reduction: When the deferral period expires (i.e., December 31, 2026), if the QOF investment was held for 5+ years, the gain included in gross income is reduced by 10%; if the investment was held for 7+ years, the gain included in gross income is reduced by 15%.

- Future Gain Exempt From Tax: When the taxpayer eventually exits the QOF, if the QOF investment was held for 10+ years, the taxpayer is permanently exempt from paying capital gains tax on the gain realized from the sale of the QOF investment (or in some cases the sale of the QOF’s individual’s assets).

A simplified example for illustrative purposes:

- Real Estate investor purchases a 1/10th partnership interest in a building on October 1, 2000, of $10M.

- Investor sells partnership interest for $50M on October 31, 2020.

- Investor invests $40M gain in a qualified opportunity zone fund on December 15, 2020.

- Investor exits opportunity zone fund on January 15 2030, for $100M

Investor receives three key benefits:

- $40M of gain realized in 2020 is deferred until 2026; assuming a 5% interest rate — the investor is $420k better off.

- The $40M gain is reduced by $4M; assuming a 20% capital gains tax rate investor saves $800k in taxes.

- Appreciation on the QOF investment of $60M is exempt from capital gains tax; assuming a 20% capital gains tax rate investor saves $12M in taxes.

Total Tax Benefits of Investing in QOF: $13.22M

Planning tip for first-time fund managers:

Setting up your partnership in one of those opportunity zones can give your HNW LPs tax deferral until 2027 and provides tax-free gains on the appreciation.

Fund managers can find a complete list of qualified opportunity zones here: https://www.cdfifund.gov/Documents/Designated%20QOZs.12.14.18.xlsx

This rule has been in place since 2017. Why should I care now?

It’s an election year!

You can only plan for what you know right now. §1400Z is the law of the land today. A new administration and Congress could wipe out this code section. Historically, tax law reform has not retroactively changed sunset provisions (i.e. the December 31, 2026 part).

This means any action related to opportunity zones in 2020 will likely provide investors with significant tax benefits.

As the example above provides — investors gain from investing in opportunity zone funds. However, the window could be closing.

Fund managers domiciled in qualified opportunity zones stand to provide their LPs massive value. For example, an opportunity zone fund with an IRR of 13% is significantly higher when considering the 20% capital gains tax savings.

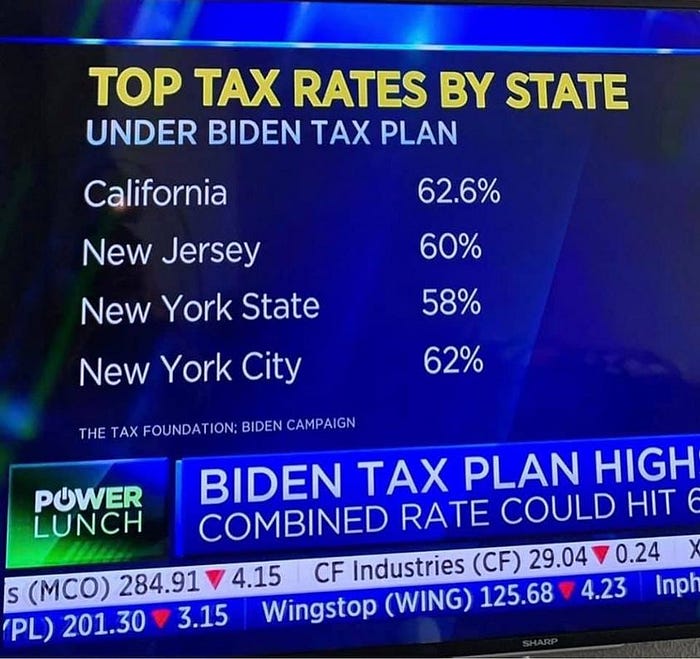

What about tax rates?

A change in administration and Congress will likely lead to tax rate changes.

If the early voting holds true a lot of investors and owner/operators are going to look to cash in on unrealized gains before tax rates increase. This will lead to a glut of M&A activity, growth rounds, and buyout exits for baby-boomer owned businesses before the end of 2020.

To the extent that they can — fund managers that have hit their carried interest or promote could be motivated to sell portfolio assets.

What’s carried interest?

Carried interest is a provision in LPAs (limited partnership agreement) that provides the GP a share in the appreciation of fund assets if a certain IRR (hurdle rate) is achieved (usually 7–10%). This appreciation is taxed as preferential capital gain income (think 20% tax rate) as opposed to ordinary income (37% tax rate).

Biden’s plan has not specifically discussed carried interest — but previously he has said he’d like to eliminate the carried interest loophole.

Both Presidents Obama and Trump campaigned on closing carried interest — yet here we are.

Any other considerations?

Presidential elections always come with potential tax law changes. As an investor or advisor, you can only plan for what you know now. Luckily taxpayers looking to tax advantage of current tax law provisions will have ~2 months after the election to finalize transactions.